Smartphone apps and online modelling tools are playing a growing role in employees’ interaction with benefits

IF YOU READ NOTHING ELSE, READ THIS…

- Originally developed as part of flexible benefit schemes, standalone modellers are becoming more common.

- Modellers and apps are most appropriate for benefits that have financial implications, such as pensions, flexible benefits, company cars or buying and selling holiday, but can also be used for other provisions.

- Until now, these have been the preserve of larger employers, but modularity is adapting them for smaller organisations.

- Employers can benefit from greater staff appreciation of benefits, lower national insurance costs through salary sacrifice arrangements, and reduced administration through online transactions.

The concept of online benefits modelling tools, which enable staff to play around with options in their perks package to determine the impact on their net pay and flexible benefits pot, is now fairly well established.

As technology evolves quickly, so does the use, and accessibility, of modelling tools. Alex Thurley-Ratcliff, a strategic consultant at Shilling Communication, says such tools have traditionally been bespoke and required a lot of investment, so their use has been restricted to larger employers. But now, the development of modular components has made them viable options for smaller employers.

And this is not the only development. “Traditionally, modelling tools have been web-based and operate in the browser using Flash or similar interactive software,” says Thurley-Ratcliff. “Recent web programming developments have enhanced the range of options available, as well as the advent of smartphones. We now see a lot more tools that are multi-platform and work well irrespective of the device.”

Smartphones are just one example of how the means of accessing benefits modellers are evolving. Brenden Mielke, product director at Thomsons Online Benefits, is seeing increasing demand from employers and employees to be able to use modelling tools on devices beyond the traditional PC. “While smartphones are becoming more popular in consumer usage, within the business context, the really exciting innovations are happening on tablets,” he says.

“This is part of a growing phenomenon known as bring your own device, and can offer an engaging experience for employees to model their pension plans, see their benefits options and costs, and understand their total reward.”

The added advantage of such tools is they allow employees to fiddle around with their benefits arrangements while on the move, such as on the way to or from work.

Apps to engage with staff

Some benefits providers and consultancies are making use of applications (apps) to engage with staff. In 2012, Towers Watson launched its TW Lifetime smartphone app to enable people to predict their own mortality using its postcode database, as a means of driving engagement with, and appreciation of, company pension schemes.

Vassos Vassou, senior consultant at Towers Watson, says: “The aim is to raise awareness of how long people might live in retirement and what they would be relying on as a pension income. The idea is that they will engage with that and share it with each other over social media.”

The app is available to anyone but can be tailored to employers’ needs, he adds.

Towers Watson has also developed a defined contribution (DC) app that allows staff in the workplace pension schemes it administers to view their current fund value, projected benefits, latest transactions and recent performance. A similar pensions modelling app released by JLT Benefit Solutions shows staff how much money they would need to contribute each month to maintain their current standard of living in retirement. JLT uses its Benpal app in one-to-one sessions with employees, and contribution levels have risen by one-third as a result, compared with similar offline schemes, says managing director Richard Roper.

Heavy financial element

The most obvious focus for apps and modelling tools is benefits with a heavy financial element, particularly pensions. Girish Menezes, a principal at Buck Consultants, says there are a number of tools that can take staff on a journey in this area, first identifying a target retirement income and then progressing to look at current levels of savings and working out the impact of making changes.

The real advantage comes when a pension modeller is used alongside other tools, such as net pay modellers or share option packages, to examine an employee’s overall saving and debt position, says Menezes. “Our real way forward is to do trust-based pensions administration and group personal pensions as well as flex and share administration, because we then offer an integrated reward portal at the end.”

Karen Partridge, chief business development officer at Anthony Hodges Consulting, says auto-enrolment is likely to drive a further wave of interest of apps and modellers because staff need to understand their retirement position. “There will be an increasing need for understanding around pension outcomes and modellers can help with this,” she says. “Financial education is also an area that will need to be addressed.”

Andrew Erhardt-Lewis, senior manager, consulting, at Deloitte says that as well as pensions, online modellers can be used for benefits such as company cars and the buying and selling of holiday, to evaluate the financial implications for the employee and any tax or national insurance savings that may be achievable via salary sacrifice arrangements.

Healthy living applications

The use of such tools is also spreading into areas that have less of an immediate financial element, such as healthy living. Analytics firm Tictrac has launched an online portal that enables people to keep track of aspects of employees’ work and home lives. Jeremy Jauncey, Tictrac’s co-founder and director of business development, says: “It looks for correlations between productivity at work in the number of emails they send and meetings they attend, and the food they eat or the amount of exercise they take.”

The platform is currently available only for consumers, but the next step is to develop a system that employers could link in with their benefits package, says Jauncey. “The natural conclusion would be for customers who engage in the platform and who start following exercise plans being offered cheaper healthcare from insurers,” he says.

Axa PPP Healthcare has now facilitated access to its Gateway platform through smartphones as well as PCs. Dr Chris Tomkins, head of personal health risk management, says: “Smartphones are a powerful supporter of behavioural change. If an employee has committed to use our five-a-day tool, it is much more powerful if they are standing in a queue thinking about buying an apple than if they are on their computer wondering if they had an apple yesterday.”

The app also includes an activity monitor so employees can track their daily exercise.

Tobin Murphy-Coles, commercial director at Lorica, gives the example of a platform that took into account people’s age, overall health and lifestyle, and suggested a range of benefits from this. “When people went on to the flexible benefits platform, rather than going through 25 benefits, they went straight to the health and wellbeing benefits if they were appropriate for them. They then did further modelling to see how much they could save each month if they were using salary sacrifice,” he says. “It is possible for any benefits permutation to be in there; it doesn’t need to be financial.”

Work-life balance

Menezes says Buck Consultants is currently looking into modelling systems that interact with employees around work-life balance and issues such as training and development, possibly to make up for their employer’s inability to offer a pay rise. “One of the things we are looking at is whether, rather than sending out a blanket email, we can analyse employees’ demographics, psychographics, work patterns and absence records, and then offer them choices,” he says.

Offering benefi ts modellers and apps has obvious advantages for employees, but there are also gains for employers. Thomsons’ Mielke says the most compelling gains are greater staff appreciation of the benefits offered by their employer, which should lead to higher levels of engagement and retention.

“Making these tools available to staff can help them really understand the full value of their package,” he says. “In tough economic times, it is important for employers to ensure they have the best staff working for them, so they have to engage them.”

CASE STUDY: SHOP DIRECT GROUP

Online modeller was a big selling point

When online retailer Shop Direct Group was seeking a provider to advise on, and host, a new pension scheme ahead of its auto-enrolment staging date in May 2013, the ability to offer staff an online modeller was a major factor in it eventually selecting Thomsons Online Benefits.

Richard Waddilove, head of employee relations and reward at Shop Direct, says: “The tool models people’s current contribution levels and their likely retirement income. Then it compares that against their target and enables them to say to what extent it will close the gap if they increase their contributions by 1 or 2%.”

The new platform, including the modeller, is currently available only to members of one of Shop Direct’s three pension schemes, but contribution levels have risen by 15% among this group since it was introduced. “That is probably a low number because it is just those people who thought they needed to save more and decided they could do so at this time,” says Waddilove.

Anyone accessing the modeller has to go through the platform’s home page, which contains a total reward statement.

VIEWPOINT: Ian McKenna, director, Finance and Technology Research Centre (F&TRC)

Tools of the trade will increase understanding of benefits

As defined contribution (DC) becomes the dominant form of workplace pensions, a wide range of tools are becoming available to help pension scheme members better understand their benefits.

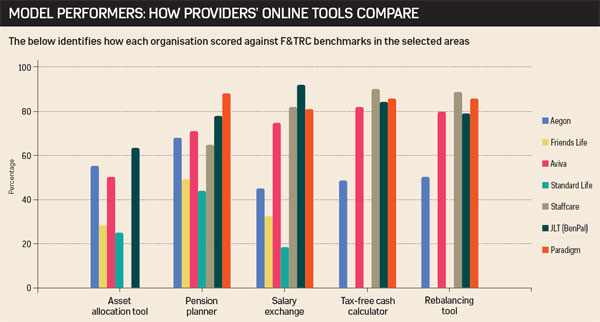

These fall into various categories. Some tools are designed to help employees better understand their own attitudes to investment and help them reach decisions about the investments in their pension. These would include: risk-profiling tools to help members understand their attitude to risk; portfolio modelling tools to help explore the type of assets held in a pension fund and whether these align with the employee’s attitude to risk; and asset allocation tools, which would help a member identify investments that match their risk profile.

Other tools are designed to help the scheme member better understand costs and benefits. For example, a pension planning tool will estimate, based on industry assumptions, how much is likely to be generated by a given contribution over the period up to retirement.

Some tools allow users to input values of other pension schemes they may hold. Salary sacrifice or exchange calculators show the additional benefit that can be achieved by giving up a portion of salary or a bonus in lieu of pension, which can reduce national insurance costs.

Other tools will enable a pension scheme member to target a particular level of income in retirement, or estimate the amount of tax-free cash they might be able to take in return for a reduced pension on retirement.

There is increasing evidence to suggest that effective use of such tools can help staff take more control over their finances and generally improve their financial wellbeing.

TYPES OF BENEFITS APP

There are a number of different mobile applications (apps) available to help employees interact with specific perks:

- Pension apps: These can help engage staff with their pension, and can include an overview of their savings, recent transactions, projected benefits and the performance of their funds.

- Healthcare apps: These can address different issues, for example, an anti-stress app that identifies stress levels and gives practical tips and advice. Also, an eyesight app that provides staff with a series of sight tests to determine if they need a full eye examination.

- Mileage claim apps: These enable employers to manage mileage claims through detailed journey logs.

- Shopping discount apps: Using these, employees can access their voluntary benefits shopping website.

- Sustainability apps: These help employers address corporate social responsibility (CSR) issues and set targets.

nifal sildenafil

definition of the side effects of sildenafil