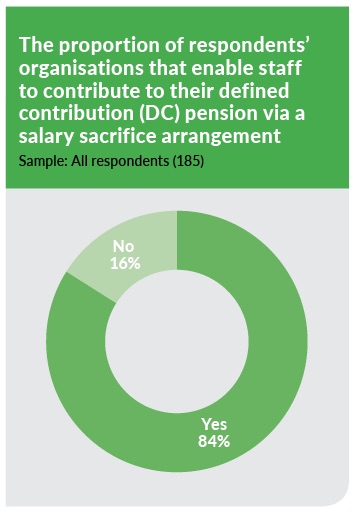

EXCLUSIVE: More than three-quarters (84%) of employer respondents allow staff to contribute to their defined contribution (DC) pension through a salary sacrifice arrangement, according to research by Employee Benefits and Staffcare.

The Employee Benefits/Staffcare Benefits research 2017, which surveyed 271 employer respondents in February-March 2017, also found that this is 10 percentage points higher than in 2016, when 74% of respondents enabled employees to contribute to their workplace pension via salary sacrifice.

Contributing to a pension via salary sacrifice appears to have grown in popularity since the introduction of auto-enrolment in October 2012. Prior to this, 44% of respondents offered this benefit in 2009, while 61% did so in 2011. Post-October 2012, 91% did so in 2013 and 87% in 2014.

Pensions are one of a handful of benefits that are exempt from the April 2017 changes to salary sacrifice, which has seen the government limit the range of benefits that attract tax and national insurance advantages when offered through a salary sacrifice arrangement.

Group personal pension plans (GPPs) remain the most common type of primary pension scheme offered by respondents’ organisations; 67% of respondents’ organisations use a GPP as their primary scheme for auto-enrolment purposes in 2017, compared to 66% in 2016. However, whereas an open defined benefit (DB) scheme was the second most popular primary scheme in 2016 (28%), this has now dropped to third place (19%). In 2017, more than a quarter (28%) of respondents’ organisations offer a stakeholder pension as their primary scheme, compared to 20% in 2016.

This corresponds with trends we have seen since the first Benefits research in 2004. Over the years, as many DB plans have closed to new entrants, there has been a corresponding rise in the proportion of respondents offering GPPs or stakeholder plans as core for employees.

The proportion of respondents introducing a GPP increased significantly following the introduction of auto-enrolment. According to the Benefits research 2014, 13% of respondents had introduced a GPP in the preceding year, compared with 5% the year before.

Former Chancellor George Osborne first announced the Lifetime individual savings account (Lisa) in the March 2016 Budget. The Lisa has been designed to encourage long-term saving, enabling individuals between the ages of 18 and 40 to open an account and save up to £4,000 a year until the age of 50. Account holders will receive a government bonus of 25% when the savings are put towards a new home or taken as retirement income from the age of 60. After the first year of launch, withdrawing savings for other purposes will attract a penalty charge.

The new savings vehicle passed into law in January 2017 after the Savings (Government Contribution) Bill received royal assent. The Lisa officially launched in April 2017, although it is not yet offered by all providers. This might partially explain why the proportion of respondents that expect their organisation to contribute to the Lisa has changed little over the last year. Just over a fifth (21%) of respondents to the Benefits research 2016 thought their organisation would contribute to the Lisa, compared to 23% in 2017.