A well-designed financial education programme can help staff improve their financial literacy and understand how such changes might affect their own financial situation, as well as generally learn how to make their pay go further.

Money worries have been a major cause of stress and anxiety for staff throughout the recession, and even now, with economic recovery beginning, many people are still struggling to make ends meet.

According to a YouGov survey of employees, Financial wellbeing: The last taboo in the workplace, published in May 2014, conducted on behalf of Barclays Corporate and Employer Solutions and Barclays Workplace Banking, one-fifth say their personal financial problems have interfered with their work.

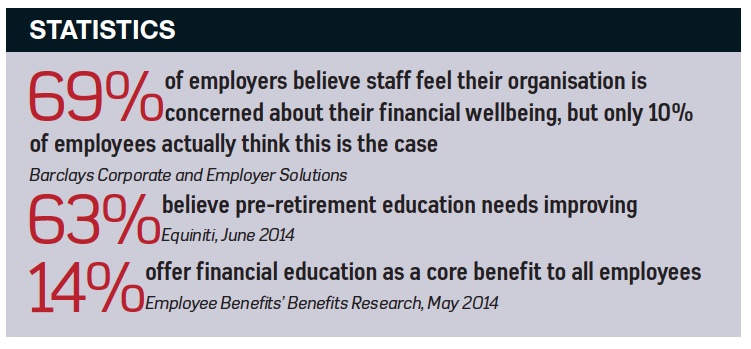

More tellingly, the report revealed a significant disconnect between employees and employers on this subject, with more than two-thirds (69%) of employers believing staff feel their employer is concerned about their financial wellbeing, but only one in 10 (10%) employees believing this.

Meanwhile, the Chartered Institute of Personnel and Development (CIPD)’s summer 2012 Employee outlook focus , based on a survey of more than 2,000 employees, found that three-quarters (73%) said their employer offered them no financial support or advice to help them understand and manage their finances better. Although only 16.9% of employers offered financial education to their employees, more than half (53.4%) offered access to debt advice, counselling or guidance.

Business case for financial education

However, with measures announced in the 2014 Budget giving defined contribution (DC) pension scheme members greater flexibility at retirement, and government calls to employers and the pensions industry to ensure employees are educated about their retirement options going forward, there is a compelling business case to implement a financial education programme.

These programmes typically provide guidance about financial benefits, including pensions, share schemes and individual savings accounts (Isas). One option for employers is to appoint a financial education provider or independent financial adviser to provide guidance in the form of workshops that cover a range of topics relevant to their particular workforce.

A further option is for employers to segment their workforce and organise tailored workshops for different employee groups to optimise the effectiveness of the programme. For example, debt management workshops could be targeted at younger staff who may be struggling with student debt.

Employers that want to offer a financial education programme should first consider the needs of their workforce and then the basis on which they are prepared to offer guidance. Do they want to work exclusively with one provider or share the workload among several providers that offer different financial specialisms?

Employee segmentation

The research analysis used for the abovementioned Barclays report applied financial health segmentation to survey respondents. This found that a significant number of employees would benefit from greater employer support in managing their day-to-day finances, as well as education about the advantages of measures such as a savings buffer.

It identified four financial health categories: comfortable, coasting, balancing and slipping. Based on this segmentation, more than half (59%) of respondents were found to be in the ‘balancing’ category, focusing on managing their current financial situation rather than saving for the future. More than one in 10 (11%) respondents, meanwhile, fell into the ‘slipping’ category, which means they have no savings and regularly spend more than they earn.

Once employers have identified which groups exist in their workforce, they can then target education programmes.

Guidance guarantee

Following the sweeping changes to the way employees will access their pension funds announced in the 2014 Budget, the government has also guaranteed that everyone who retires in a DC pension will be offered free, impartial, face-to-face advice about their choices at the point of retirement. It is not yet clear how this guidance will be delivered, although the government will provide £20 million over the next two years to develop the initiative.

Pension providers and trust-based pension schemes will have a new duty to offer this ‘guidance guarantee’.

Providers and trust-based schemes will also be required to ensure the guidance given follows a set of robust standards, which will focus on helping DC members to understand the choices available to them at retirement, engage with products and providers confidently, and access professional independent financial advice.

However, the extent to which many employees are unaware of the changes and what these will mean for their personal situation has been identified in a number of polls carried out following the Budget.

For example, research published by MetLife in May found that more than one in three employees approaching retirement were unaware of the Budget pension reforms, and that 35% are either unaware or unsure about the pensions overhaul due in April 2015, which will enable retirement savers in DC schemes to access their money however and whenever they like from the age of 55.

A survey by Capita Employee Benefits, also in May, found that a quarter (28%) of employees in workplace DC pension schemes have no idea how much their pension is worth. Also, more than half (54%) do not know how much they need to save for their retirement. A similar proportion feel pensions jargon makes retirement planning harder, and 48% say they would be more likely to save into a pension if they understood how it worked.

These surveys show that many employees are not actively engaged with their pension, so there is a need for some form of help and support to make sense of their retirement funds and how to plan for this life event.

However, financial education does not always come cheap, which makes provision challenging, particularly for smaller employers. Some organisations are minimising cost by offering financial advice on a voluntary basis, while others offer employer-funded advice to those most in need, such as retirees. Others target only senior managers and executives by providing financial advice offered by an independent financial adviser (IFA).

But employers must remember that financial advice must only be given by a registered financial adviser.

Retail distribution review

The retail distribution review (RDR), introduced in January 2013, was aimed at preventing intermediaries from making biased product recommendations based on the providers that pay the most commission. This means that financial advice and education from IFAs and benefits consultants is now charged on a fee, rather than commission, basis, which may deter some employers from making a long-term commitment to financial education.

The facts

What is financial education?

Workplace financial education involves employers, or a third-party provider, educating employees about financial benefits, such as pensions and share plans, but it can also include individual savings accounts (Isas) and tax planning, and how to use these perks to optimise their financial wellbeing.

Financial education can be delivered to staff through one-to-one sessions and group workshops, and covers a range of topics, such as investment guidance and retirement planning. Online programmes can also be arranged, using webinars and video-conferencing technologies, such as Skype and Google Hangouts.

What are the origins of financial education?

Financial education programmes first began to emerge in the 1970s, triggered by mass redundancies, when many long-serving employees received sizeable lump-sum payments and needed some financial guidance on how best to use their redundancy packages. Initially, this focused mainly on pensions before evolving into the much broader offerings seen today.

Where can employers get more information?

More information is available through Employee Benefits ’ financial education channel

What are the legal implications?

Employers are prohibited from giving employees financial advice. Only Financial Conduct Authority-registered advisers are permitted to do so.

What are the costs involved?

A financial education programme can be expensive for employers, although costs will vary depending on an employer’s size and the provider it chooses. Prices can start from less than £1 per employee per year.

What are the tax issues?

HM Revenue and Customs regards individual financial education as a benefit in kind, with the tax charged generally on the cost to the employer providing the benefit. There are exceptions, for example for pensions advice costing below £150 per employee per year.

What is the annual spend on financial education?

No official figures are available on the annual spend on financial education, but employers can spend as much as £3,500 per employee per year on independent financial advice.

Which are the main providers?

The biggest providers include Anthony Hodges Consulting, Clarity, Close Brothers Asset Management, Friends Life, Jelf Employee Benefits, Life Academy, Lorica Employee Benefits, Mattioli Woods, Money Advice Service, Nudge Global, Origen, Towers Watson and Wealth at Work.

Agree with most of the comments in the article.

However, the fact of the matter is that despite all the communication and information over so many years we still find that people struggle with financial literacy. Worryingly, the case for well directed financial awareness that is person centric and meets their real their needs throughout life still remains an issue even in 2014.

All concerned need to face up to the challenges and look in the mirror and ask why is it still a problem? What should we have done better before? How best to rectify the problem going forward? Not point in throwing good money after bad!

Wladek Koch, Director, Life Planning Association

The plan would greatly cut the complicated procedure currently required for Chinese companies to file initial public offerings (IPOs) on the mainland and Frankfurt. Many netizens however, could not care less about these outpourings of public remorse which invariably follow arrest. Celebrities, they say, need to seriously rethink their behavior instead of simply crying crocodile tears when they are caught. “I can only lie down or sit, and can’t do anything else. My family has to do all the work while I just sit there being useless,” said Yang. tn pas cher france Shanghaiprosecutors’ offices have filed charges against 327 people in relation to 249 drug-related cases this year.

Du 27 juin au 13 juillet la commune de Spolète accueille, comme chaque année la Festival Des Deux Mondes, l’un des plus importants rendez-vous internationaux dédiés au théatre, à la danse et à la musique. Mis à part les deux semaines de spectacles, cette 57e édition, accueillant des cultures et des expressions artistiques différentes, propose un programme riche en événements de grande qualité. Al contrario era ben noto il fondatore dei Boko Haram, il defunto capo spirituale Ustaz Muhammad Yusuf, quando la setta era più nota con il nome del leader, la Yusufia. In realtà politici e militari avevano fatto leva sulla sharia come strumento di pressione nei confronti del governo centrale. hollister france Il lungo contenzioso con il Cile non ha mai trovato soluzione; e neppure il negoziato tra il presidente cileno Michelle Bachelet e quello boliviano Evo Morales, pur nell’alveo di uno spirito di collaborazione positivo, si è tradotto in un accordo. Il dossier è sul tavolo dei giudici della Corte internazionale de L’Aja. hollister pas cher un segno che nonostante gli aiuti europei e gli interventi legislativi di sostegno, la crisi dei mutui ancora non è passata. ?I dati statistici ancora non si sentono nelle strade?, dice Manuel Arias Maldonado, politologo dell’Università di Malaga.

Il partito, nato nel 1995 (proprio l’anno di ingresso di Helsinki nell’Unione europea) dalle ceneri del Partito rurale finlandese, si definisce un movimento di centro. In realtà combina caratteristiche proprie della destra – nazionalismo, difesa dei valori tradizionali – con posizioni di sinistra, soprattutto in campo economico. Breeden ha finora a disposizione soltanto una frazione della somma teoricamente in gioco: 4 miliardi di dollari. Altri 2 miliardi sono stati pagati dagli eredi dell’investiorre Jeffry Picower, investitore e amico di Madoff. La svolta anti-austerity dei socialdemocratici chaussures louboutin femmes pas cher L’Angola è stata la terza tappa del tour africano di Li Keqiang, dopo Etiopia e Nigeria (dove ha preso parte al World Economic Forum) e prima del Kenya, dove Li è in visita oggi. Prestiti in cambio di petrolio chaussures louboutin femmes pas cher Nuove elezioni sono previste per il 20 luglio, anche se la data non è stata ancora ufficializzata. Rischio di nuovi scontri di piazza La decisione dell’Alta Corte rischia di riaccendere le proteste di piazza che vedono fronteggiarsi le camicie rosse.

Ma il programma, secondo i critici, è sotto-finanziato. Si era parlato di 140 milioni di euro in tre anni. Quest’anno a budget sono stati messi 33 milioni di euro. Tenuto conto della spesa in servizi, che comprende il riscaldamento, i consumi sono però lievitati complessivamente del 3%, soltanto in relativo calo rispetto al 3,3% del quarto trimestre del 2013. nike air jordan Mentre i curdi, concentrati in una regione autonoma ricca di oro nero e di gas, sono sempre più tentati, soprattutto con la crisi siriana, dal miraggio di distaccarsi da un governo centrale visto soltanto come un impedimento per arrivare un giorno, forse, allo stato unito del Kurdistan. nike air max 95 Non a caso il presidente Jonathan fa appello anche a Barack Obama per avere aiuto. E ora dopo avere vissuto ai margini, i Boko Haram tentano il salto di qualità con un ciclo di attacchi e rappresaglie tanto spettacolari quanto cruenti che hanno l’obiettivo di colpire al cuore la capitale e destabilizzare l’esecutivo.

Per questo Axelrod nelle sue prime dichiarazioni dopo la nomina a ?consigliere strategico? ha sottolineato di avere acccettato l’incarico perché stima il leader del partito. ?Nel corso di numerose conversazioni con Ed Miliband nell’ultimo anno sono rimasto colpito dalla forza delle sue idee, dalla potenza della sua visione e dal suo profondo impegno nel risolvere i problemi fondamentali che la Gran Bretagna deve affrontare?, ha dichiarato. mulberry factory shop L’India si prepara a sacrificare un altro Gandhi, Rahul, stavolta solo politicamente. Al delfino della dinastia Nehru-Gandhi, che è una cosa sola con il partito di maggioranza, il Congresso, tocca l’ingrato ruolo di vittima predestinata nelle elezioni in corso.

The campaign for pandas’ conservation began on January 17, 1953, when the “first” wild panda was found in Yutang, a town near the city of Dujiangyan. Then, the panda was rescued and relocated to Chengdu’s Futoushan Breeding Facility at the Chengdu Zoo, the precursor to the Chengdu Research Base of Giant Panda Breeding (CRBGPB). In 2013, the number of new malignant tumor cases hit 40,307, up 3.22 percent from the previous year. “It’s good for poor children in remote mountainous areas to come in contact with different people with different background. It helps them grow up,” he adds. nike tn pas cher With a stable career and a happy family life in Ningxia, Ahmed has come to regard the region as his second home.

Il primo, dal titolo “L’amico del figlio”, è stato presentato oggi alla trasmissione televisiva di Rai 1 “Uno Mattina” sarà disponibile sul canale You Tube Polizia di Stato, sul sito web Polizia di Stato e sulle pagine facebook delle Questure che hanno già operativo il servizio (Roma – Milano – Aosta Proprio ieri il presidente ha minacciato di “espropriare” e “confiscare” le aziende che non dimostrino di aver applicato la cosiddetta “legge del prezzo giusto” – che fissa a un massimo del 30% il margine di guadagno – entro il 10 febbraio, minancciando i “settori della borghesia” a non “sottovalutare il potere del popolo”. hollister femme Alle parole si associa una situazione che sul campo rimane tesa: le truppe russe schierate al confine orientale dell’Ucraina (circa 40mila uomini in tutto) hanno avviato esercitazioni militari nella regione di Rostov. hollister en france Chiediamo al ministo del Turismo greco, signora Olga Kefalogianni, in questi giorni in vista in Italia, e che ricopre un ruolo importante nel governo presieduto da Antinis Samaras, se pensa che quest’anno verrà raggiunto un nuovo record.

Solo il 2% dei bambini di età inferiore ai 15 mesi viene vaccinato mentre l’accesso all’istruzione è molto limitato: l’80% dei giovani è analfabeta e il 35% dei musulmani non ha mai frequentato una scuola, neppure quella coranica. Solo il 2% dei bambini di età inferiore ai 15 mesi viene vaccinato mentre l’accesso all’istruzione è molto limitato: l’80% dei giovani è analfabeta e il 35% dei musulmani non ha mai frequentato una scuola, neppure quella coranica. louboutin pas cher homme eleggerà il mese prossimo un nuovo leader che sostituirà il premier uscente Jyrki Katainen, sia perché le attuali politiche economiche hanno depresso l’economia di Helsinki, in contrazione in tre degli ultimi cinque anni (quest’anno si prevede un +0.2%) e con una disoccupazione salita all’8,5 per cento. chaussure louboutin pas cher Cipro dal 1974 resta un’isola divisa dall’ultimo muro d’Europa. Ma oggi la Turchia è stata condannata dalla Corte europea dei diritti umani di Starsburgo a versare entro tre mesi 90 milioni di euro a Cipro per risarcire i familiari delle vittime delle operazioni militari condotte dalle forze di Ankara tra il luglio e l’agosto 1974 contro i greco-ciprioti residenti nella penisola di Karpaz.

Nella lista nera del dipartimento di Stato Usa come terrorista, con una taglia sulla testa da 7 milioni di dollari, Shekau, che in una rara intervista si definisce uno studioso e un intellettuale, ha più le stimmate del capo banda che del predicatore, con le astuzie tipiche del latitante: E i due conflitti nel cuore del Medio Oriente, siriano e iracheno, sono intanto diventati come vasi comunicanti con la presenza di Al Qaida e dei gruppi jihadisti collegati sia in Iraq che in Siria. basket air jordan mentre sarà riformata la Sanità, anche con la creazione di un Fondo per la ricerca medica da 20 miliardi di dollari che sarà finanziato con una quota consistente dei ticket pagati dagli assistiti. cheap tn shoes Con la decisione di oggi i giudici hanno stabilito che la Turchia dovrà versare al governo cipriota 30 milioni di euro per risarcire i familiari delle persone scomparse durante le operazioni militari e altri 60 milioni ai residenti greco ciprioti della penisola di Karpaz, per la violazione dei loro diritti in seguito alla divisione dell’isola.

sembra che quello ritratto nei filmati non sia lui ma una sorta di controfigura che gli somiglia. Basta questa però a seminare in questi giorni il terrore e a sgretolare l’immagine di un governo nigeriano impotente e corrotto. mulberry handbags Questa giustizia egiziana intesa come killing field ne ha fatta un’altra: ha anche messo fuori legge il Movimento 6 Aprile. E’ il gruppo giovanile democratico che tre anni fa iniziò la rivolta di piazza Tahrir, i cui leaders sono già in carcere da mesi a subire pene pesanti a causa di accuse inesistenti.

http://www.biblibre.com/en/blog/afi-and-biblibre-annonce-bokeh-first-4g-documentary-portal

http://bartlebyediting.com/services/

http://www.3pforum.com/topsites/index.php?a=join

http://www.resellerratings.com/store/survey/Touchboards

http://www.bankruptcylawreview.com/blog/subaru-recall-weakens-gm-defense-brake-line-rust-maintenance-issue

A person essentially assist to make severely articles I would state. This is the first time I frequented your web page and thus far? I amazed with the research you made to make this actual publish incredible. Fantastic job! neues bayern trikot I couldn’t resist commenting. Very well written! maillot du psg pour enfant Heya i am for the primary time here. I came across this board and I to find It truly helpful & it helped me out much. I am hoping to provide one thing back and aid others like you aided me.