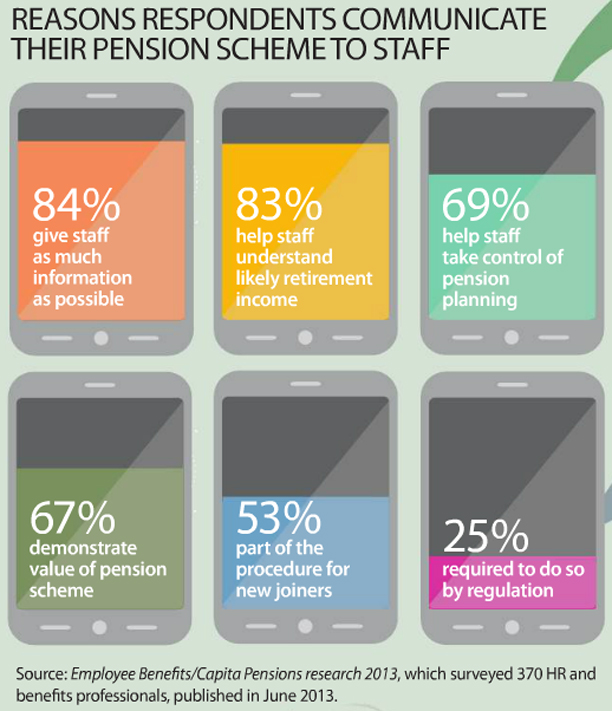

48 Analysis news Financial education Pensions How much do staff need to contribute for a comfortable retirement?