Tax-efficient employee benefits offer potential savings for both employers and staff, with some perks free of income tax, employee national insurance (NI), employer NI, or a combination of these.

If you read nothing else, read this…

- Salary sacrifice arrangements can increase employee engagement with benefits.

- Employers can use NI savings from salary sacrifice arrangements to help fund pensions auto-enrolment, introduce new benefits, or cover the cost of benefits technology.

- It is important to communicate the value of tax-efficient benefits to employees.

These savings can be used to fund various extras, such as new benefits, to fund pensions auto-enrolment or to cover the cost of benefits technology. But employers should not take them for granted.

Sarah Minter, reward consultant at Major Reward, says: “Employers are using the money they save on NI to spend on technology, or will use it to fund a new benefit for employees, perhaps an extra 1% pension contribution or putting in a health cash plan.”

For example, Barbon Insurance funded a flexible benefits scheme from the employer NI savings it made through salary sacrifice pension arrangements.

Minter, formerly reward manager at the insurer, adds: “An employer cannot be expected to pay for every single benefit that employees want, but if every benefit available is via salary sacrifice, then the employer’s savings will go up and up.”

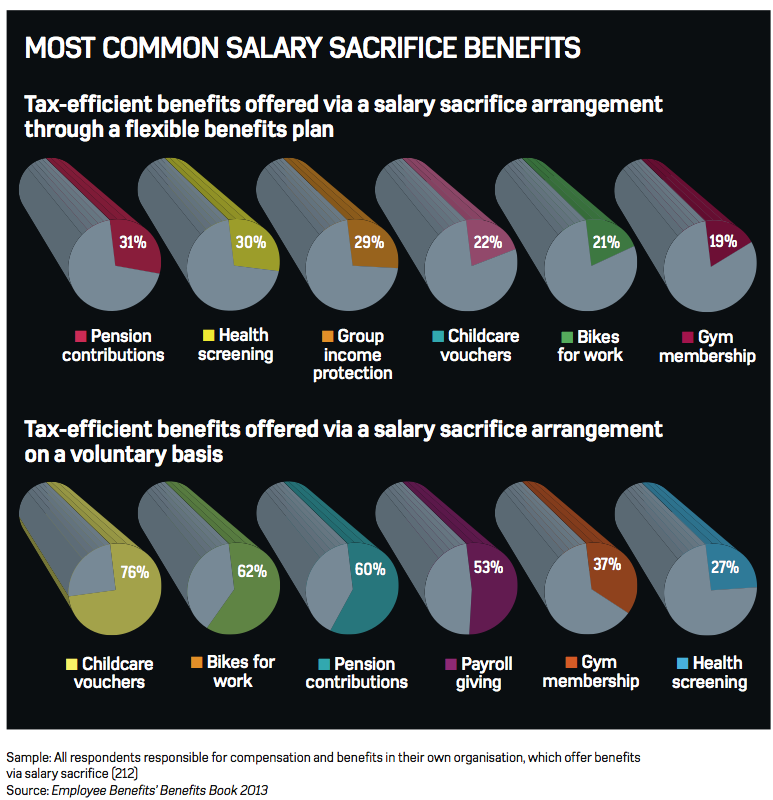

Salary sacrifice arrangements

Salary sacrifice is a contractual agreement whereby an employee gives up part of their gross pay in return for a non-cash benefit from their employer. Pensions salary sacrifice is one of the most common ways to make tax savings.

Richard Maitland, director in people services at KPMG, says: “A lot of employers are looking at pensions salary sacrifice, because it applies to so many employees, particularly in the light of auto-enrolment. If they don’t provide [salary sacrifice] already, that is the best way to start.”

Health screening , when provided only once a year, is not classed as a benefit in kind, but tax savings from the perk can be maximised. Minter explains: “If an employer has a health cash plan, they can link those two together.

“[At Barbon], we used to put the health screening through as one benefit, but then employees could reclaim the cost of it through the health cash plan anyway, which makes it doubly tax-efficient.”

Graham Farquhar, employment tax partner at EY, thinks mobile phones are one of the best benefits employers can provide tax-efficiently. “If you provide an employer mobile phone, there is no benefit, even though the employee might use it 100% for private use,” he says. ”But if an employee buys a mobile phone and then gets reimbursed, that is tax-efficient.”

Benefits that typically have lower take-up, such as dental and medical cover for employees’ dependants or access to energy-efficient company cars, are still worth being made available via salary sacrifice arrangements , because they are highly valued by staff.

Maitland adds: “It costs money to set up these schemes, but because of the volume of take-up, it doesn’t always drive significant savings. But they are very worth doing, because of the employee engagement that comes off the back of it.”

Childcare voucher changes

Childcare vouchers are one of the most commonly offered tax-efficient benefits, but the scheme is set to change from autumn 2015. In his 2014 Budget, Chancellor George Osborne confirmed the system will be replaced by a tax-free childcare scheme on up to £2,000 on childcare costs. This will be rolled out to all eligible families with children under the age 12 in its first year. Unlike vouchers, the scheme will not rely on employers offering it.

Staff will also be able to continue to use existing childcare voucher schemes, as long as they do not change employers, but the current system will be closed to new entrants.

David Heaton, tax partner at Baker Tilly, says: “Pretty much everybody was better off [with childcare vouchers], especially when they were offered via salary sacrifice. But [the new system] will not work with salary sacrifice.

“I suspect a lot of existing schemes for tax-free childcare will be withdrawn, because there won’t be enough people in them to justify the expense of running them.”

Employee communications

If an employer was to bring in a salary sacrifice arrangement, whether for its pension scheme or lifestyle benefits, it is important to provide a full explanation to employees.

Claire Sheridan, head of flexible benefits at Capita Employee Benefits, says: “Part of the general salary sacrifice communications, especially when an employer first introduces it, is what it is as a concept, why is it being introduced and what the benefit is for employees, not just from a tax and NI perspective.”

This is a powerful message to bring to the board as well, says Sheridan. “That is one area [organisations] can show in their business case: that they are introducing a scheme that is good for them as an employer and good for the employee. Most employers that come to us are looking to be cost-neutral as a minimum and salary sacrifice is a way of doing that.”

Minter sees salary sacrifice arrangements as a full circle of cost-efficiencies. “If an employer introduced a salary sacrifice benefit, then the employee is saving money, but they need to ensure the employee understands the advantages,” she says. “Using the benefit then drives higher engagement , which produces better savings for the employer, which gives them more money to spend on more benefits.

“A lot of employers think they can’t afford to put in benefits. Actually, if they’re using the tax breaks properly and doing it tax-efficiently , then they most definitely can.”

Case study: Martindale Pharma reinvests salary sacrifice savings in staff benefits

Martindale Pharma used the savings it made from adding a salary sacrifice arrangement to its group personal pension scheme to fund the cost of auto-enrolment and to improve its healthcare benefits.

The organisation introduced pensions salary sacrifice in April 2013. Keith Baker, compensation and benefits manager at Martindale Pharma, says: “We wanted to take advantage of the national insurance (NI) savings for employees and the employer. It is a quick win and had an impact on some other areas, such as auto-enrolment and healthcare.”

The concept of salary sacrifice was communicated to the employer’s 400 staff with the help of benefits adviser Secondsight, which held a series of presentations for small groups of staff, and included personalised calculations within its information packs for employees.

“It gave them specific details on how salary sacrifice would impact their own net pay,” says Baker. “Within the presentations, we encouraged them to reinvest that saving to increase their pension contributions with no impact on their net pay and, ultimately, make a difference to their retirement income.”

The organisation’s initial NI saving was £21,000, much more than it had expected. The savings, which have continued to rise, have been used to fund auto-enrolment . Baker adds: “We were given costs in terms of the pension provider, access to their hub for assessments and all the statutory communication that is required.

“We made sure that was covered by some of the cost savings we made. But because it was actually more than we anticipated, we were able to put that into some other areas as well.”

These other areas included changing the organisation’s private medical insurance scheme from an underwritten plan to a medical-history-disregarded plan at no extra cost, and improving the terms available on its life assurance cover.

“It wasn’t just pension members who were benefiting from the savings,” says Baker. “It was broadened out across as many employees as we could touch.”

John Whiting: Employee benefits tax system needs modernising

The Office of Tax Simplification (OTS) was set up to study areas of the tax system and make recommendations to the Chancellor on simplifying rules and procedures. Recently, we have spent a lot of time looking at employee benefits and expenses, and published a major report in January 2014.

This is the product of talking to a lot of employers, advisers, individuals and front-line HM Revenue and Customs (HMRC)] staff about what they find difficult or time-consuming.

Our small team of private-sector secondees has particularly been looking for areas where the rules have not kept pace with changing working patterns.

Our recommendations included: the payrolling of benefits should be available to employers that wish to use it; pay-as-you-earn (PAYE) settlement agreements should be greatly widened in terms of what they can cover with no prior HMRC approval; the introduction of a set amount for trivial benefits, probably £50, below which there would be no tax liability; and the abolition of the £8,500 higher-paid [income tax] threshold.

On travel and subsistence, we recommended looking properly at a new system that basically exempts any costs covered by employers.

In the meantime, travel for the first 24 months of a temporary workplace should qualify in all cases; employees should have just one ‘permanent workplace’; and there should be better definitions around home working.

In the long term, we also want real progress on bringing PAYE and NI contributions together, and argue for a major review so we get to a rule that says ‘no benefit = no tax’.

If ministers decide to take [the recommendations] forward, and there will be a consultation if they do, we think our ideas would make a real difference, modernising the system and cutting out a lot of wasteful work.

As a target, maybe 40,000 annual P11Ds instead of 4.4 million? Meanwhile, we’re looking at accommodation benefits and termination payments. Comments welcome.

John Whiting is tax director at the Office for Tax Simplification (OTS)