It has been almost a year since the retail distribution review (RDR) came into effect on 31 December 2012 and, with the the Department for Work and Pensions’ (DWP) consultation on a charges cap closing on 28 November, the workplace pension charges landscape continues to change.

If you read nothing else, read this…

- The Department for Work and Pensions’ consultation on pension charges includes the introduction of a 0.75% cap on charges, a ban on active-member discounts and an extension of the ban on consultancy charging to include all DC pensions, rather than just auto-enrolment schemes.

- Charges should not be looked at in isolation, but in the context of contribution levels, investment returns and pre-retirement education.

- Employers should know what their pension scheme’s charges and costs are, and should renegotiate these at least every two years.

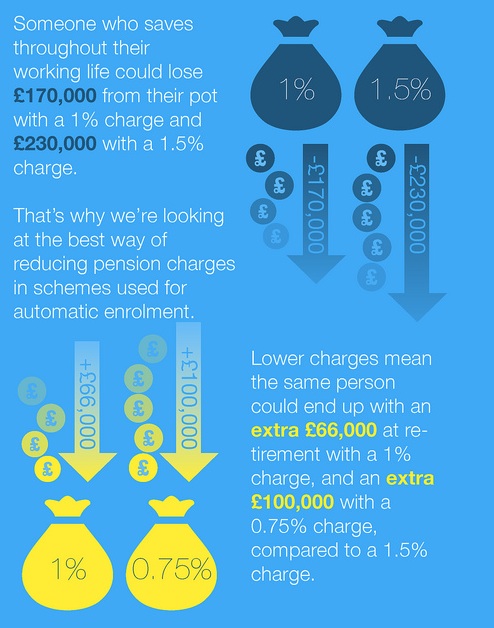

The DWP’s proposals include the introduction of a 0.75% cap on charges. Michelle Cracknell, chief executive officer at the Pensions Advisory Service, points out that the proposed cap would be specifically for default funds.

“That is important from an employer’s perspective,” she says. “How many of your staff would you expect to go into the default fund? Because if a provider tries to look at the totality to make sure it meets its profit margins, the number of people going into default funds with capped charges will make a difference.”

Charges modelling

The consultation includes some modelling around pension charges. It shows that if a pension scheme member pays an annual management charge (AMC) of 1% instead of 0.75% throughout their savings lifetime, their pension pot would be worth 6% less.

Mark Winstanley, corporate pensions director at Jelf Employee Benefits, says: “What would happen if the individual paying the 0.75% got more support around financial education to help them understand what they should pay into a pension? An increase from an 8% to 9% contribution would equate to an increase of 12% a year [in the projected fund]. It would more than outweigh the impact of the charges.

“That is quite important, because everyone is looking at charges in isolation. We have got to take it in the context of everything, in terms of contribution levels, investment returns and more education when people retire.”

Active-member discounts

The DWP’s consultation followed the Office of Fair Trading’s (OFT) market study on DC pensions, which was published in September. One of the key recommendations in the OFT report, which has also been addressed in the government’s consultation, was to ban active-member discounts, whereby an ex-employee pays a higher fee than an active employee.

John Lawson, head of policy at Aviva, says: “I would expect providers to re-label schemes to a profit-neutral price between the active member’s price and the leaver’s price. That would mean charges will go up for active members, but really we don’t have a lot of choice if the government mandates this change.”

Will Aiken, senior consultant at Towers Watson, says the OFT has recommended that active-member discounts and commission should be permissible for auto-enrolment schemes, but only after a forward-looking date. “So, at the moment, an employer could use a scheme that generates its commission for auto-enrolment,” he says. “But, at some yet-to-be-determined date in the future, if a scheme was paying commission, it would not be auto-enrolment compliant.

“This leads us to some strange no-man’s land where, if an employer had its staging date now, commission is okay, but if it has it in a year’s time, it won’t be okay.

“Similarly, active-member discounts would be OK if an employer is staging at the moment, but won’t be okay at some future stage. Having seen what happened around the churning of schemes ahead of RDR last year, I imagine some people will be bringing their staging dates forward, so commission will be generated.”

Consultancy charging

In September, legislation to ban consultancy charging on auto-enrolment pension schemes took effect, which means an employer cannot receive advice under an agreement with a third party, other than a trustee, provider or scheme manager, and pay for that advice out of its employees’ pension pots or contributions.

The DWP’s consultation recommends an extension of the ban on consultancy charging to all DC schemes. Aviva’s Lawson says: “I would expect new members’ commission to feed through to an effective ban on all commission in the long term. The members will pay a lower charge, but an employer would have to pay for advice directly as a fee.”

A new industry code of conduct for the disclosure of pension charges, which was drawn up by the Association of British Insurers and the National Association of Pension Funds, will be implemented in the summer of 2014 for schemes that are newly established for auto-enrolment, and for older workplace pension plans by 31 December 2015.

Lawson adds: “If I were an employer, I would encourage my provider to start disclosing those costs on the same terms. It’s the easiest way for employees to see how much they are being charged and it is the easiest way to compare charges across different providers and different schemes.”

Standard framework

The DWP consultation also proposes the introduction of a standard framework for the ongoing disclosure of costs, charges and services to pension members. The Pensions Advisory Service’s Cracknell says: “As we all know, the more information provided, the less it is read. Disclosure is a real issue: to get the level of disclosure right, that the information to members is sufficient so they understand the charges, but not too much that they don’t read any of it.”

Employers should ensure they are aware of what their pension scheme’s charges and costs are, and should renegotiate these at least every two years. Towers Watson’s Aiken says: “There is a lot of pressure anyway to disclose what your charges are, so it is important to know what you are paying, both from AMC level and total expense ratio, and probably also understanding what the transactional charges are.

“Charges have been generally drifting down over the last 10 years. It doesn’t take too long before what an employer is paying is out of line. If they haven’t negotiated for four or five years, they’re probably overpaying for the services they’re receiving.”

This year has seen an almost continuous flux in the legislation around pension charges, all heading in the right direction, but there is still plenty of work to be done.

Cracknell adds: “There are still hidden charges and unnecessary surprises, either at the fund level or at the policy level. The more we can move away from that, the better. And I would love to see a set of simple and fair charges. We’re better than we were in 2001, but we’re not there yet.”

Read also How transparent are benefits charging structures? at: http://bit.ly/16oDgjh

Definitions

- Annual management charge (AMC) is the fee paid to a pension fund manager for their investment services and expertise.

- Additional expenses are fund-specific and relate to some of the, often external, expenses incurred by a fund manager in offering a fund.

- Total expenses ratio (TER) can be considered as the sum total of the AMC and additional expenses. It is defined as the total average cost over a year, divided by the average net assets.

- Transaction charges might include stamp duty, brokerage fees, market impact costs and performance fees.

- Commission is a payment made by a provider to a consultant or independent financial adviser that is generally directly related to the size of contributions.

Source: Pension charges explained: navigating the hidden costs, Towers Watson

Key dates

- 14 September 2013: Legislation to ban consultancy charges on auto-enrolment pension schemes came into effect.

- September 2013: The Office of Fair Trading published its report on the defined contribution (DC) pensions market, including a focus on dealing with old and/or high-charging schemes, and on improving the quality of information available on costs and charges.

- 30 October 2013: The DWP published a consultation on pension charges.

- 28 November 2013: The DWP’s consultation closes. It will be followed by government proposals on charges and scheme quality.

- Summer 2014: The Association of British Insurers’ code of conduct for disclosing information on the charges made on workplace pensions will be implemented for schemes newly established for auto-enrolment.

- 31 December 2015: ABI code of conduct will be implemented for older workplace pension schemes.

Pension charges infographic

Source: Better workplace pensions: a consultation on charging, published by the DWP in October 2013

Thank you for your article. Really Great.