The number of women preparing adequately for retirement is at an all-time low and remains well behind the preparation levels of their male counterparts, according to research by Scottish Widows.

The ninth annual Scottish Widows 2013 Women and pensions report, which surveyed 5,000 people, found that just 40% of women, compared to 49% of men, are prepared adequately for later life, a drop from 42% in 2012 and 50% in 2011.

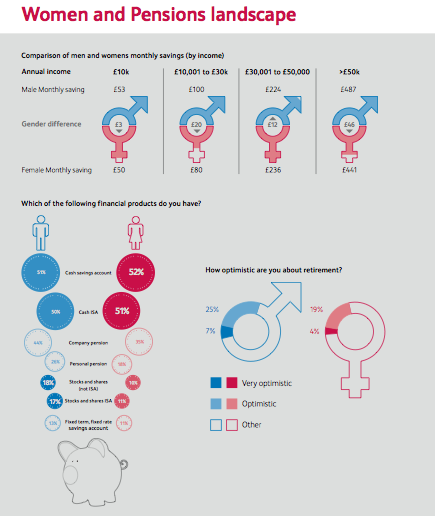

The research found that more than a third (37%) of women have no pension, while the same applies for more than a quarter (27%) of men.

Female respondents who are saving are putting aside £182 a month on average, well below the average amount of £260 among male respondents. This creates a gender pension savings gap of nearly £1,000 a year.

The research found that different lifestyle factors are impacting the savings habits of women at different ages. For instance, women in their 20s were found to be tied down by short-term financial pressures and are prioritising living expenses (42%), paying off debts (26%), travel and holidays (23%) or saving for a property (18%) above saving for retirement.

More than half (54%) of those aged between 22 and 29 do not have a pension, compared to 37% of the general female population.

Only 50% of women in their 30s work full-time compared with 81% of men of the same age, which means 30-something women bring in an average gross income of £19,200, way behind the £28,700 of the average 30-something man. Career breaks and cutting back on hours have a knock-on effect on women’s ability to save, with women in their 30s only saving £87 a month on average towards retirement, outside of pension and property investments. This is compared with the £151 that their male counterparts are saving each month outside of pensions and property.

By the time women reach their 40s, their financial priorities have changed, with almost a quarter (23%) of those aged between 40 and 49 prioritising financially supporting their children over retirement saving in the last five years. Nearly one in four (24%) also said they expect their partner’s income to help support them in retirement, despite the fact that 79% do not know what their partner would be entitled to from their pension fund if they were to separate.

Despite their proximity to retirement age, paying off debt is still a priority for women in their 50s, with 24% of women of this age still considering paying off debt a bigger priority than saving for retirement. Women in their 50s still owe an average amount of £11,400, slightly higher than the £11,000 of average debt among women in their 40s.

Lynn Graves, head of business development, corporate pensions at Scottish Widows, said: “It is worrying to see that women are continuing to lag behind men in retirement savings. The number of women preparing adequately for retirement has dropped from last year to a record low.

“This growing gender gap in retirement savings means that women are facing an ever increasing shortfall when it comes to retiring and must act now to ensure they will not be left exposed in later life.

“We have identified the different barriers that prevent women from saving at every life stage, helping us to see where this gender savings gap is coming from and understand how best we can support women to help them overcome these barriers.

“The pensions industry, government and employers need to work together to raise awareness of the unique lifestyle pressures that take their toll on women’s savings at different ages and help women prioritise their pensions.”

Where a husband is working and their wife is working part-time or taking a career break, they can still make pension contributions on behalf of their partner, using the universal pension allowance. This is good financial planning because it makes sense to have two incomes in retirement rather than one; that way you take advantage of both partner’s tax-free personal allowance.

In theory, a couple could have a pension income of £18,880 a year (2 x £9,440), which is entirely tax free, and the Coalition is set to push the personal allowance to £10,000 and beyond, making this type of planning even more attractive.

There is more that can be done to help women enjoy a comparable standard of retirement provision to men. The government can raise the universal pension allowance, which has been stuck at £3,600 since 2001 and is falling woefully behind against rising prices. This is an important allowance widely used by non-earning spouses, those taking career breaks and children. Had this increased by RPI inflation it would now be over £5,289.

Employers should be encouraged to talk to their employees about the benefits of auto-enrolment, to encourage as many lower earners as possible to opt in to their workplace pension scheme and take advantage of their employer’s contributions.

It is extremely disappointing to note from the report that, despite all the advances that have been made in women’s rights and in society generally, the number of women preparing adequately for retirement is at an all-time low and remains well below that of their male counterparts.

Historically, of course, women have tended to fare much worse than men in relation to pensions. Traditionally, men went out to work and were the bread winners, while women stayed at home to bring up children and/or only worked part-time, missing out on both state and private pension provision in consequence. Although very different lifestyle practices now exist they are clearly not enough to bridge the gap between men and women in every respect and further help and support needs to be given to women in looking ahead to their position in later life.

Because the state pension will provide a substantial part of many people’s retirement income, all women should be encouraged to find out and review at regular intervals their record of national insurance (NI) contributions so as to ensure they are on track to get a full state pension at the appropriate time. Gaps can often be made good to their financial advantage by buying back missing years through voluntary contributions.

In terms of private pension provision, women should also be given every encouragement to seriously consider joining any employer-sponsored scheme that may be available to them so as to secure a pension in their own right and relieve the dependency they may have to have on their husband’s or partner’s income to support themselves in later life. If, as may often be the case, their level of earnings is not high enough for them to be automatically enrolled into their employer’s scheme, they should bear in mind that they can usually always ask to be voluntarily enrolled and hopefully receive an employer’s contribution into the scheme in consequence.

And finally, at retirement age itself, all married couples planning to exchange their pension pot(s) for an annuity should contemplate buying one which contains provision for a spouse’s pension. Although a partner’s demise is not something many want to think about, it is a fact that whether through divorce or widowhood, many women end up on their own and the continuation of a pension is something that could be very valuable at that difficult time and for the rest of their life.

The situation where women are in some way treated almost as second-class citizens belongs in the past and certainly should not exist in the 21st century. Greater equality in pension provision is an important part of the change that we need to achieve as soon as possible.